Student Loan Debt Crisis in 2021: Original Study & Meta-Analysis

Student Loan Debt Crisis in 2021: Original Study & Meta-Analysis

In the last 50 years, college tuition costs in the US increased by 340%. Today, 70% of students take a loan to afford college. We analyze what it means for them.

Certified Professional Resume Writer, Career Expert

FML.

So read the headline of HuffPost’s Highline 2017 piece detailing how badly the Millennials had been screwed by the 2008 recession and the resulting job insecurity, housing crisis, healthcare system inefficacy, and more. Juxtapose all that with soaring college tuition costs (up by 340% since 1970, adjusted for inflation), and you get a pretty grim picture.

As of 2017, less than a third of Millennials had any college degree which doesn’t sound surprising at all—they simply couldn’t afford one.

In the four years that followed, a lot has changed in the economy. 2018 saw a major tipping point in the job market: for the first time ever, there were more open jobs in the US than candidates to fill them. January 2020 brought the lowest unemployment rate since 1969. All that caused more young people than ever to enroll in college: 40% in 2020, compared to 32% in 2017.

Yes, 70% of them got student loans, averaging $30,000, yet, borrowing money seemed to make more sense than ever. For the first time in years, the job market seemed on our side. We would bounce back.

And then, the COVID-19 pandemic struck, unemployment spiked to almost 15% and, all of a sudden, we’re facing the scariest financial future of any generation since the Great Depression—again.

Amidst this reality, there are 45 million Americans owing roughly $1.6 trillion in student loans.

In this study, we’re aiming to find out how they cope, what sacrifices they need to make, and what the future looks like. We surveyed 500+ American student loan borrowers and here’s what they told us.

Expectations vs. Reality

As mentioned earlier, an average cost of a student loan is at about $30,000. You don’t just throw 30k you don’t even have at something unless there’s some serious motivation behind it.

We asked student loan borrowers why they decided to go to college in the first place:

51% did so to achieve a higher earning potential,

28% wanted to pursue their passions and interests,

15% didn’t know what else to do with their lives.

Interestingly, among those who enrolled in college but ended up dropping out, the proportion of students who entered only because they had no idea what else to do was twice as high as in the general population: 30%.

We also found a strong correlation between one’s current salary and their motivation for pursuing higher education—

The more American borrowers currently earn, the more likely they were to have enrolled for a higher earning potential, which seems like a self-fulfilling prophecy: if you go in for the money, you’ll end up chasing it, and you’re more likely to get what you want.

68% of respondents who make over $70,000 a year went to college to achieve better financial perspectives,

52% of those making between $40,000 and $70,000,

52% between $25,000 and $40,000,

only 34% below $25,000.

Similarly, people who studied vocational or applied sciences were more likely to go to college to be able to earn more (69%), than those who studied humanities or social sciences (41%)—not surprising, considering that jobs in engineering or tech are amongst the best-paid professions in the US.

A very disturbing finding of our survey was that only 50% of American student loan borrowers ended up in jobs that even require a college degree, including just 32% of people who currently make between $25,000 and $40,000 a year and just 18% of those making less than $25,000.

How the hell so? Did 22.5 million people just forget what they even borrowed the money for? Sadly, not.

Imagine it’s 2010 and you just graduated. The economy is in ruins. There are hundreds of thousands of unemployed people with tons of experience under their belts fighting over the few jobs left that match their qualifications—you’re up against them with just your degree and no real on-the-job skills to show on your resume.

Of course you’re not getting hired there. But—

You need money to repay your loan so you settle for some general labor position and hope the job market turns around. Eventually, it does, but then you’re left with a dated degree and no relevant experience. The new fresh grads are taking those entry-level positions you might consider applying for.

You have no choice but to stick around. You can’t pursue graduate education because, guess what, you have your old student loan to repay and you don’t want a new, six-figure one. And, yes, you’re likely in the below-40k-a-year range.

At the same time, only 26% of respondents said they sacrificed a job that offered more fulfillment and purpose for one with a higher paycheck.

Interestingly, it was more common amongst those who entered college for a higher earning potential (31%), than those who associated higher education with pursuing their passions (22%). Again, it seems that if you go to college to make more money, later on, you’re more prepared to give up on ideals for $$$. If personal development, rather than financial benefits, is what drives you while at university, you’re more likely to stay that way once you graduate.

Generally speaking, 48% of our respondents said they were satisfied with their current jobs: those earning the most (over $70,000 a year) were most likely to claim so (64%), the self-employed ones—least so (30%).

All the job-seeking and career dilemmas considered, we asked American student loan borrowers the big question: in hindsight, was it all worth it? Was the degree you got worth the cost? Overall, only 30% of respondents said it was.

A peculiar trend we discovered was that the longer you’ve worked, the less likely you are to think a college degree was worth the spend. Amongst borrowers with less than 5 years of experience, 45% said they got their money’s worth out of college, 33% of people with 6 to 10 years’ experience thought so, and only 25% of those who spent 11 years or more in the workforce.

The reason? It’s difficult to find hard data to analyze that pattern but perhaps it’s easier to see the benefits of college education when applying for entry-level jobs—this is where your degree can give you an edge. Later on, your experience becomes a more relevant factor in hiring or promoting.

Related to that data is another finding of our survey: 51% of student loan borrowers think companies in their field should be looking for competency, such as on-the-job training, or apprenticeship programs, instead of requiring a college degree. This opinion is most prevalent amongst those who never finished their degree (75%).

What Student Debt Means to Borrowers

There you are. Facing a dozen-or-so years of paying back your student loan. The very perspective itself is scary—numerous studies have shown that any sort of financial strain is associated with symptoms of depression, anxiety, and physical health problems.

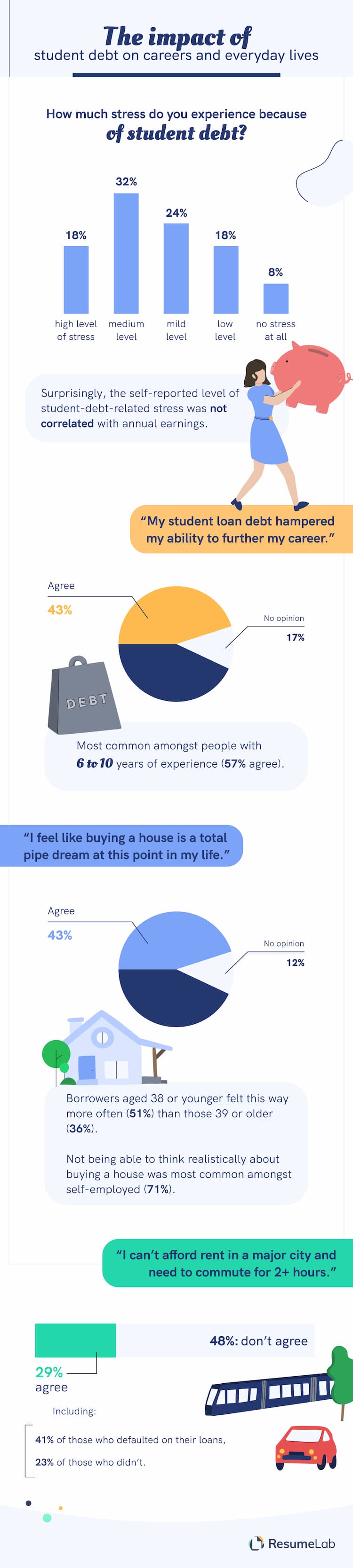

We wanted to know what degree of stress American borrowers experience because of their student loan debt: 74% of respondents said they experienced medium- to severe-level stress in their day-to-day lives.

Intertwined with earnings or not, stress can be a debilitating factor in anyone’s life. We asked our respondents whether they thought their student loans hampered their ability to further their careers: 43% agreed; 40% disagreed. A significantly higher percentage of students who defaulted on their loans agreed with the statement (54%), compared to those who didn’t (39%).

A key indicator of financial stability—the ability to buy a house—seems a distant reality to many American student loan borrowers. 51% of them aged 38 or younger consider buying a house “a total pipe dream,” at this point in their lives. Such a feeling is most common amongst self-employed borrowers (71%).

Paying rent, arguably a basic need in everyday life, doesn’t come easy to all borrowers, either. 29% of respondents, including 41% of those who defaulted on their loans, said they couldn’t afford rent in any major city and needed to commute for 2+ hours a day.

Evaluating Past Choices and Looking Into the Future

33% of our respondents regret not having delayed their enrollment for a year or more to travel, volunteer, or save money. On the face of it, it doesn’t seem like too many. A more granular approach to the data reveals some interesting insights, though:

Out of borrowers who went to college mostly because “they didn’t know what else to do,” 55% regret not having taken a gap year beforehand.

Similarly, 55% of those borrowers who ended up dropping out wish they had taken a year off before college.

It paints a sad picture of a calamity that could have been avoided—had it not been for an overwhelming pressure pushing young people to go to college no matter what, many of those individuals would have lived happier, less stressful lives today.

26% of our respondents said they failed to continue their education on a graduate level due to the financial strain of a student loan. Unsurprisingly, it was most common amongst borrowers who defaulted on their loans: 41%.

Career regrets aside, we wanted to learn what American student loan borrowers thought about the current, pandemic-related trends in higher education: namely, colleges switching to online teaching despite heavy technological limitations (only 5% of an average pre-COVID-19 college budget was allocated to IT).

More borrowers agreed (48%) than disagreed (33%) that obtaining a degree online is just as valuable as on campus. Interestingly, 67% of those who dropped out thought so!

(At the same time, only 18% of respondents took a non-university online course within the last 12 months.)

Methodology and Limitations

For this study, we collected answers from 517 American student loan borrowers via Amazon's Mechanical Turk. The data rely on online self-reports after eligibility screening. Respondents consisted of 53% females and 47% males. 6% of respondents were 24 or younger, 62% aged 25–38, 29% aged 39–58, and 3% 59 or older.

Given the gender and age makeup of our large sample, the study can be generalized to the entire population.

This self-report study investigated American student loan borrowers’ attitudes toward their debts, decision-making factors, and outlooks for the future. Respondents were asked 14 close-ended questions, and 10 scale-based questions. To help ensure that respondents took our survey seriously, all respondents were required to identify and correctly answer two attention-check questions.

Some questions and responses have been rephrased or condensed for clarity and ease of understanding for readers. In some cases, the percentages presented may not add up to 100 percent; depending on the case, this is either due to rounding or due to responses of “neither/uncertain/unknown” not being presented.

As experience is subjective, we understand that some participants and their answers might be affected by recency, attribution, exaggeration, self-selection, non-response, or voluntary response bias.

Feel free to share our study! The graphics and content found here are available for noncommercial reuse. Just make sure to link back to this page to give the authors proper credit.

With vast expertise in interview strategies and career development, Michael is a job expert with a focus on writing perfect resumes, acing interviews, and improving employability skills. His mission is to help you tell the story behind your career and reinforce your professional brand by coaching you to create outstanding job application documents. More than one million readers read his career advice every month. For ResumeLab, Michael uses his connections to help you thrive in your career. From fellow career experts and insiders from all industries—LinkedIn strategists, communications consultants, scientists, entrepreneurs, digital nomads, or even FBI agents—to share their unique insights and help you make the most of your career.

![A Boss From Hell [2020 Study]](https://cdn-images.resumelab.com/pages/bad_boss_listing.jpg)